2024 Fourth Quarter Commentary: Economic Recap and Market Summary

THE YEAR THE 20S ROARED

Download Commentary | Watch the Highlights

The economic picture over 2024 was that of a maturing but healthy cyclical expansion, propelled by productivity gains and accented by an election that will likely have a material influence over fiscal policy and deregulation. The markets reacted with enthusiasm, and valuations now look stretched relative to history.

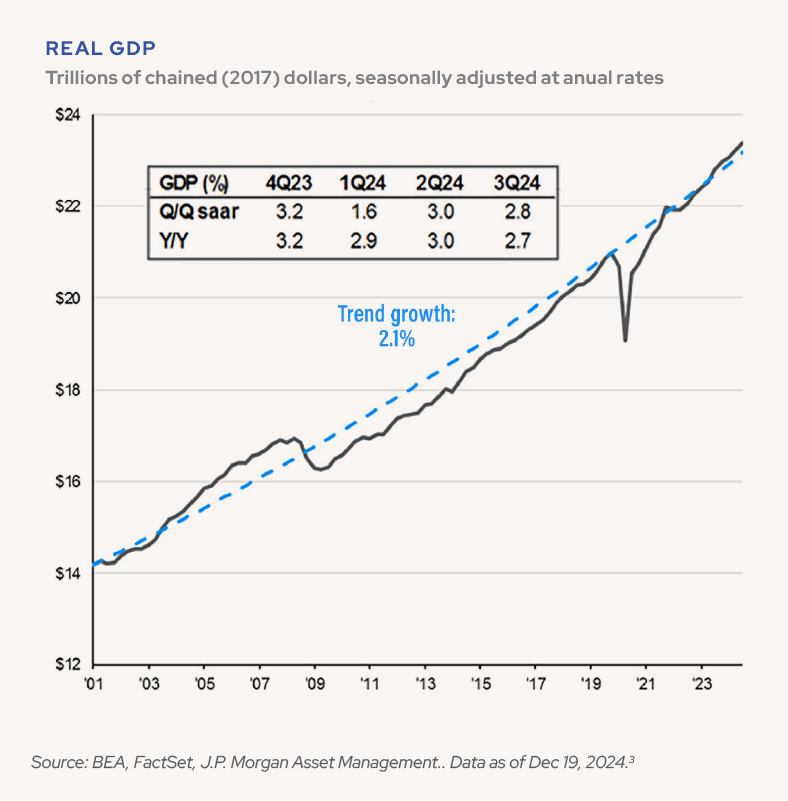

The fourth quarter underscored a theme that has resonated throughout the past twelve months: 2024 was a spectacular year for the U.S. economy. Inflation has stabilized, and unemployment has remained within bounds. The economy is expected to print a 2.7% growth rate for the calendar year, trouncing the original consensus estimate of 1.7%.[1],[2] Whatever your preferred euphemism for satisfying both ends of the Fed’s dual mandate – “immaculate disinflation,” “soft landing,” or something else – that outcome appears to be in hand.

Source: BEA, FactSet, J.P. Morgan Asset Management.. Data as of Dec 19, 2024.[3]

The Fed itself seemed to agree, lowering interest rates three times, totaling 1% between September and December. Donald Trump’s re-election in November kickstarted a late rally in risk assets that pushed the entire year’s gains well past the realm of investor expectations. Notwithstanding a minor parry from the Federal Reserve in mid-December, investors are now eager to turn the page into 2025.

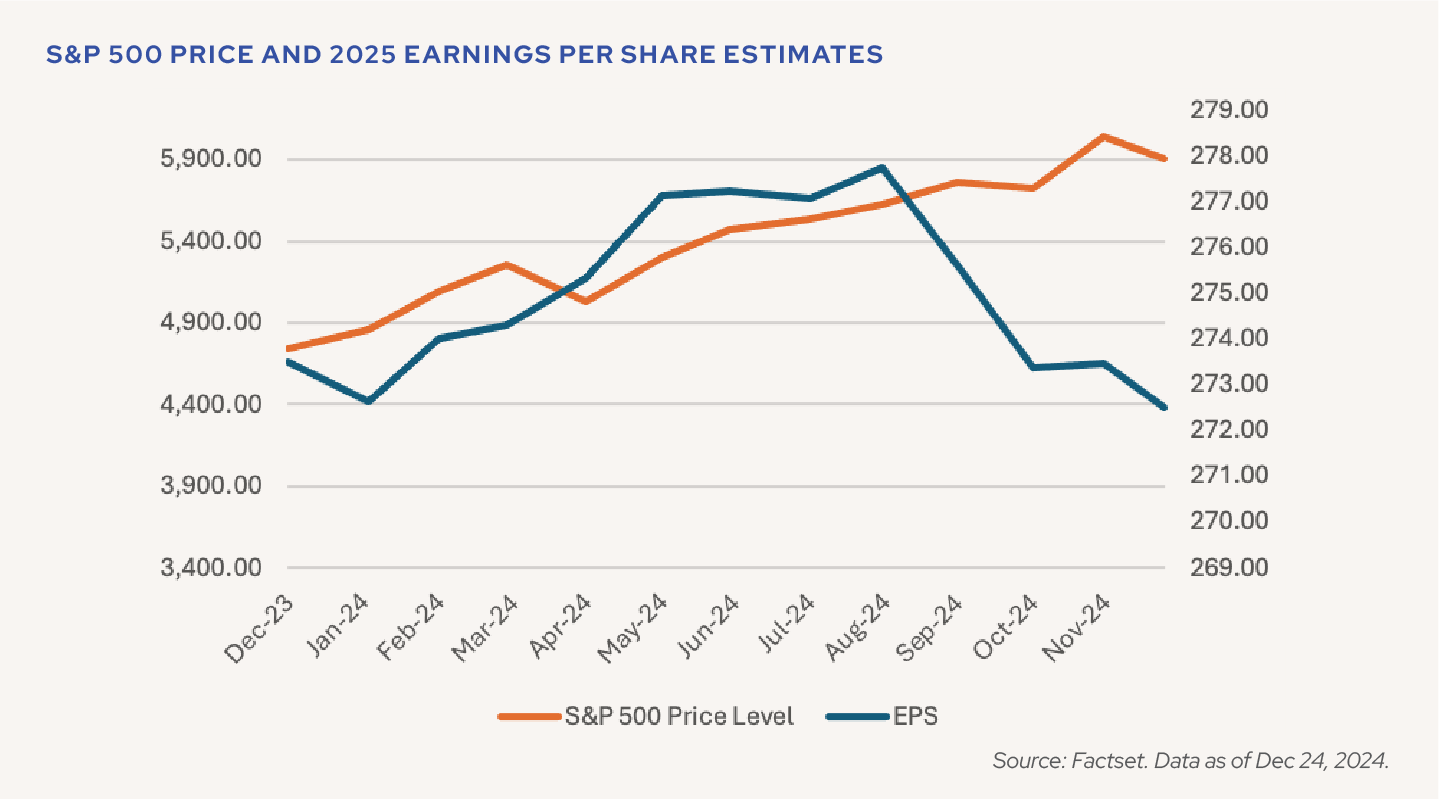

In fact, some might argue that the markets already have. The S&P 500 ended the year up 25.0%, notching the first back-to-back period of +20% returns since 1997-1998. Other than the 2020-2021 meme stock rally, valuations haven’t been this rich since the tech bubble: at 21.5x, the market is currently trading at forward P/E multiples 1.4 standard deviations above 30-year average valuations. This late surge can’t be attributed to improving fundamentals, either: forward-looking earnings estimates for the S&P 500 in 2025 peaked back in August and have since fallen roughly 2% due to revised forecasts. A stock market that has priced in an accommodating economic backdrop at high valuations creates risks heading into 2025; while signs are still pointing towards a healthy year, it could be a bumpy ride.

Source: Factset. Data as of Dec 24, 2024.

That being said, a lot happened over the past year that merits our attention beyond fourth quarter earnings revisions. Much like WWI and the Spanish Influenza gave rise to the “Roaring Twenties,” we find ourselves navigating the aftermath of a global pandemic, geopolitical reshuffling, and economic turbulence. Then, as now, societies faced rapid change: inflation surged before moderating, technological innovation flourished, and financial markets exhibited both exuberance and excess. As we close the chapter on 2024, the parallels invite reflection, not as a forecast but as a reminder of how periods of disruption can create fertile ground for both risk and opportunity.

Q4 2024 WRAPPED

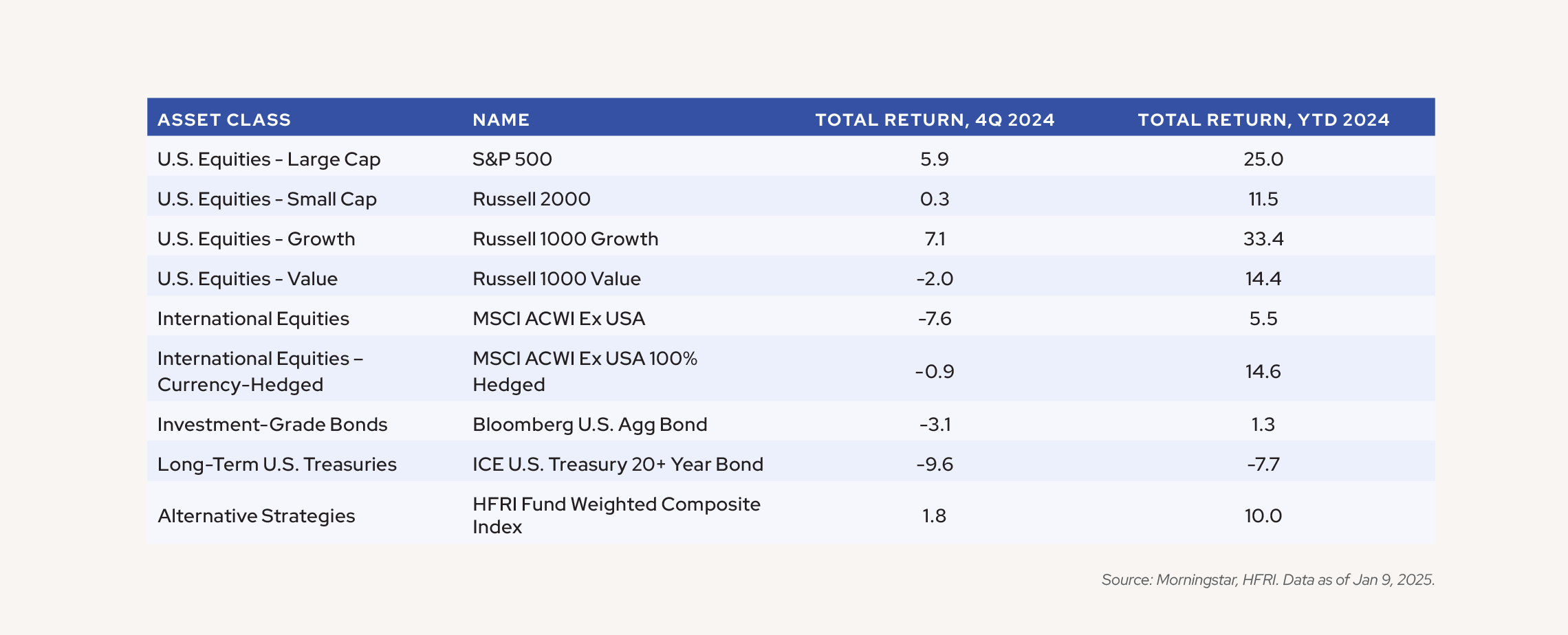

As was the case for much of the year, U.S. equity markets had a spectacular quarter, but those gains were highly concentrated.

The Magnificent Seven reasserted their dominance yet again and for the year, represented 57% of the return of the S&P 500. Meanwhile, small caps landed flat, bonds stumbled, and international markets entered a full-on slump.

Source: Morningstar, HFRI. Data as of Jan 9, 2025.

The relative dominance of this one small cohort continues to push the envelope of index constitution. The weight of the top five stocks in the S&P 500 is roughly 27.1%, the highest it’s been since at least 1967. To address this index concentration, we believe that it’s prudent to introduce some risk management in the large cap growth space, which is why we’ve added active management to U.S. large cap equity.

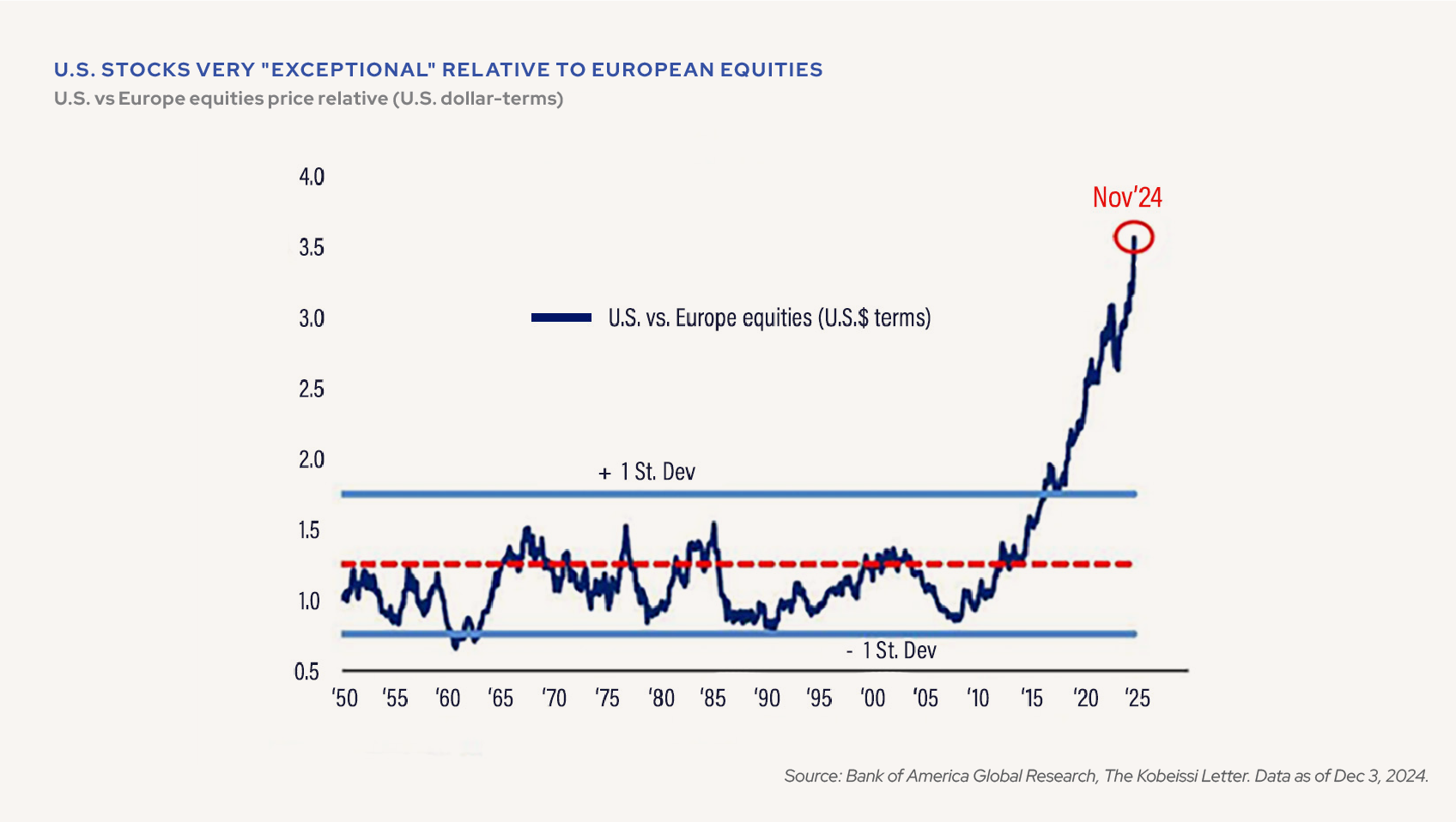

International equities lost ground to the U.S.

Buoyed in part by Donald Trump’s election to the presidency in November, the U.S. extended its dominance over financial assets at the expense of the rest of the world. Relative to Europe for instance, the U.S.’s market concentration is now close to four standard deviations away from the norm.

Source: Bank of America Global Research, The Kobeissi Letter. Data as of Dec 3, 2024.

Beyond an excellent year in the equity markets, there’s another factor at play driving the current market concentration: the greenback’s remarkable rally against other currencies. Since 2000, our current period is the closest the dollar has come to overtaking the strength that it had prior to the 1985 Plaza Accord, a trade agreement formed with the express purpose of devaluing the U.S. Dollar.

The effect is substantial. The MSCI EAFE Index – a broad proxy for developed international markets – fell 8.1% in the fourth quarter. Meanwhile, the currency-hedged version of that index gained 0.1% – an eight-percentage point delta. In emerging markets, the effect was similar, though not as extreme: -8.0% vs. -4.3%.

Going forward, this effect may be partially offset by the incoming administration’s aversion to a strong dollar. However, with tariffs and tax cuts likely to be a facet of the political discourse throughout 2025, it’s also possible that the dollar could continue to strengthen in the near term, which would be a headwind for unhedged international allocations. In either case, there’s bound to be unpredictability around trade that makes these waters difficult to navigate.

Bond markets digested Fed guidance and the election

Downstream of tariffs and other potential policy decisions that could re-ignite inflation, hopes for rate cuts in 2025 fizzled as the year wound down. Trump’s victory and the Fed’s hawkish Federal Open Market Committee (FOMC) guidance nudged yields up and bond prices down.[4] Between September 30 and December 31, markets revised their year-end 2025 forecasts for interest rates from 3.2% to 3.9% – still lower than June’s 4.4% reading, but enough to cause the Bloomberg Barclays U.S. Aggregate index to fall 3.1% for the quarter and end the year effectively flat.[5],[6] The yield on the 10-year U.S. Treasury now stands at 4.6% as of last reading, from 3.6% as of September 30.[7] That means that as the Federal Reserve has cut short-term rates by one percentage point, long-term rates rose by roughly the same amount.

Source: St. Louis Fed. Data as of Jan 2, 2025.

The reason is simple: even as it trims policy rates, the Fed has continued to guide towards a more gradual cutting cycle with a higher terminal rate.[8] We’re of the view that this current rally in yields may not have gone far enough. A combination of tariffs and a tougher stance on immigration, coupled with existing dynamics in the real estate market, could cause inflation to reignite, implying that the current runup in yields may not be finished. Escalating geopolitical tensions in the middle east and between Russia and other state actors could aggravate energy price volatility further, and ultimately cause prices to rise, which could serve as another exogenous source of inflation. That being said, the U.S. now produces more oil than any other country and the Organization of the Petroleum Exporting Countries (OPEC) has continued to serve as a lid on supply.

Our strategy recognizes these risks and causes us to seek areas of the bond market that offer compelling return opportunities without taking on excess duration risk.

Many alternative strategies, like trend following and event-driven, didn’t work, but multi-strategy hedge funds stayed the course

Tried-and-true alternative strategies also struggled throughout the quarter. The entire Wilshire Liquid Alternatives complex was down across the board. Managed futures, which gained 10.1% through March 2024, ultimately ended the year down -5.7% as markets turned choppy.[9] Event-driven strategies also faced headwinds as M&A activity slowed and deal durations lengthened.

We would not be surprised if near-term headwinds in event-driven strategies start to unwind with a new Federal Trade Commission (FTC) administration on the horizon. Importantly, other areas of the liquid alternatives space – notably convertible arbitrage – have offered compelling risk-adjusted returns in a higher rate environment, meaning we’re not forced to rely exclusively on strategies such as managed futures and event driven to drive returns in excess of the bond markets.

Multi-strategy hedge funds excelled in 2024, with most flagship strategies delivering low double-digit returns.[10] Despite the sterling returns, interest in the multi-strategy space diminished, as many premier firms distributed capital back to investors and other investors chose to redeem. Through Q3 2024, the asset class had net outflows totaling $31 billion, the first time since 2017 that more money went out than came in. We believe this represents a compelling entry point for the asset class, and multi-strategy hedge funds remain one of the highest-conviction investment areas on our platform today.

Meanwhile, interest in private markets surged

At the same time a small number of stocks contributed the majority of public market returns and premier hedge funds returned capital, private markets saw record fundraising. The top seven publicly traded private managers originated $423.6 billion in private credit over the trailing twelve months, up from $194.1 billion in the prior period. Private equity secondaries also raised a record-breaking $88 billion YTD through Q3.[11]

Source: Pitchbook. Data as of Dec. 2, 2024.

The unprecedented fundraising of private markets investments in the wealth channel has understandably made some observers skittish, particularly as it relates to private credit. Indeed, the asset class does introduce risk: it’s not possible to produce 9-10% yields without it. However, we don’t believe this is a reason to avoid the asset class entirely, but rather to allocate to it prudently – by treating private credit as an equity-like source of risk and focusing our due diligence efforts on ensuring that our managers have rigorous underwriting and the muscle to withstand distress scenarios. Private investments are illiquid, and we believe it’s critical to ensure that clients understand these are long-term investments and allocate accordingly.

2024 UNWRAPPED

Economic backdrop in the U.S. is pretty good, across cyclical indicators leaving consumers flush with cash and deploying it after ever-narrowing opportunities

Economic resilience in the U.S. continues to drive consumer spending, which grew at 3.7% in the third quarter.[12] Unemployment remains at 4.2%, with the Fed projecting a peak of just 4.3%. Real wage growth and pandemic-era savings cushions have allowed households to shore up balance sheets. Of course, not everyone is able to participate – lower income consumers and the young, both of whom are more rate-sensitive, are struggling to keep pace. Overall though, households in the U.S. are wealthier, less indebted, more likely to be employed, and higher paid (on a real basis). Services account for nearly 70% of consumption and 85% of private-sector employment, anchoring the economy.

Source: BlackRock, Bureau of Economic Analysis. Data as of Nov 30, 2024.

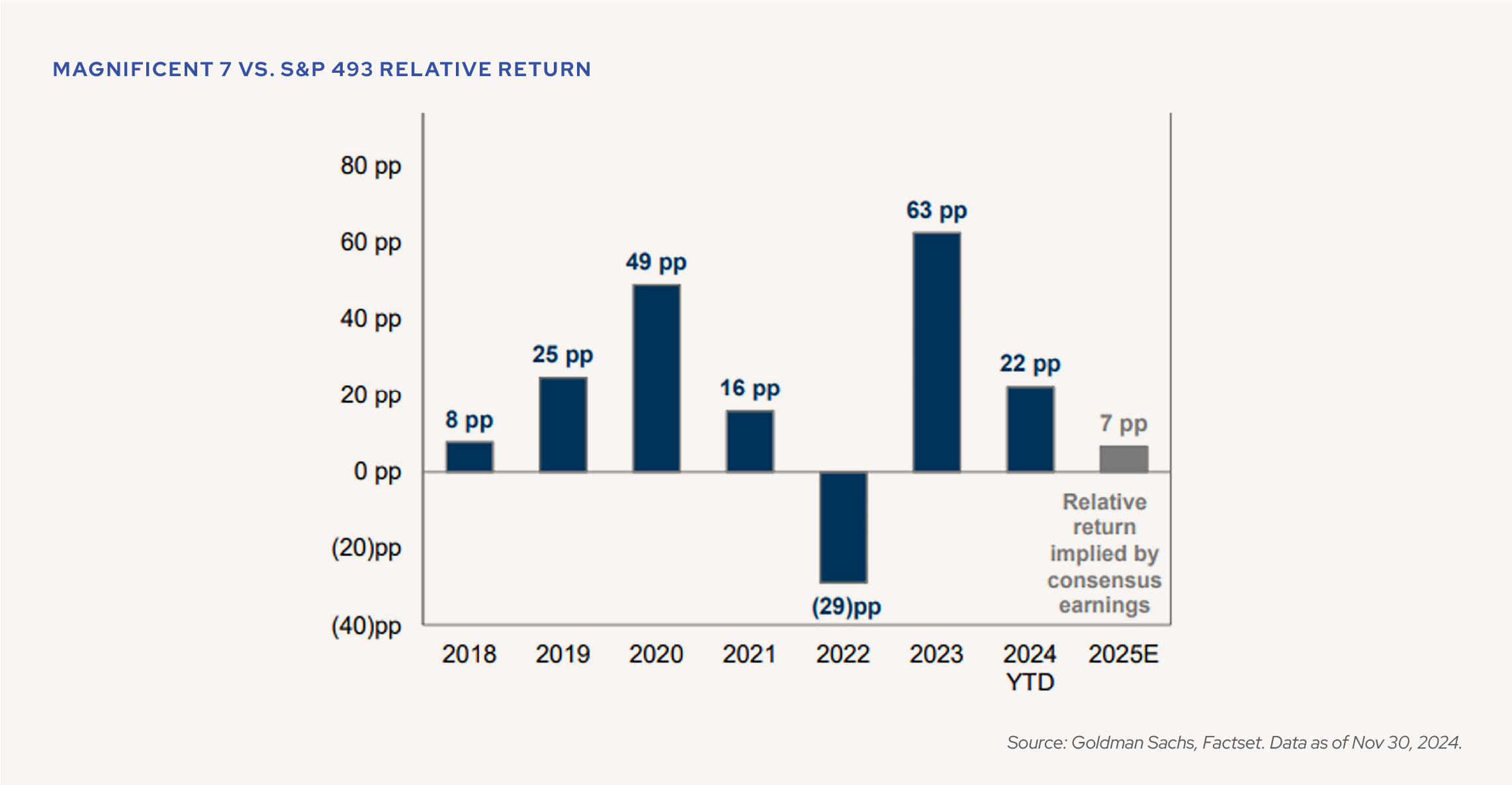

Lower levels of debt and higher real yields also mean that investors are flush with cash – total assets in money market vehicles today are close to $10 trillion.[13] By and large, investors are choosing to funnel that cash into the equity markets, chasing ever-fewer opportunities. In particular, interest has coalesced around artificial intelligence during a paradigm-shifting year in the infrastructure that supports the technology. This AI fever was spurred along by the so-called “hyperscalers” – specifically Amazon, Microsoft, Google, and Meta – who grew their capex by roughly 56% in 2024.[14] Along with Nvidia, Apple, and Tesla, these companies (collectively known as the Mag 7) account for more than half of the S&P 500’s return in 2024, as they did in 2022 and 2023. As we look ahead to 2025, forward earnings expectations rely on improved conditions for the rest of the U.S. equity market while reflecting less stratospheric expectations for that group.

Source: Goldman Sachs, Factset. Data as of Nov 30, 2024.

Looking at the S&P 500 as a whole, forecasters expect 14.8% earnings growth, after delivering 9.5% earnings growth in 2024.[15] Although analysts tend to get earnings growth directionally right, close to 15% improvement might be a touch optimistic. With 2.0-2.5% Gross Domestic Product (GDP) growth expected for next year, it is difficult to see how the market could deliver materially better results without an external event of some sort, such as unanticipated rate cuts, deregulation, or another paradigm shift in artificial intelligence.

Hang on, you might say – AI can’t carry the entire economy. Point well taken. It has certainly demonstrated the ability to carry the large cap segment of the stock market though. That’s because the public market opportunity set today relative to history is greatly diminished. Even tech, an area dominated by giants, proves that case in a point: 96% of all software companies today are private.[16] This concentration is evident in credit, too: net issuance excluding Treasuries is trending at the lowest levels in at least five years, and the discount that corporate bonds trade at relative to Treasuries hasn’t been this low since 2005.

These dynamics are partly why we remain focused on allocating across markets both public and private in order to get a truly representative and diversifying sample of investments. As competition has intensified within broad-based private markets funds, managers have started introducing niche products that we believe carry higher alpha potential. We remain focused on these types of opportunities going forward.

The federal deficit has a lot of people concerned, but maybe not as concerned as they should be

Across the world, demographics continue to pose a major challenge. In general, the world’s population is growing, but at a decelerating clip. Even the United States is starting to come under scrutiny, albeit for a second-order effect of an aging population: the fiscal deficit. Deficit spending continues to run at 6-8% of GDP, a level the U.S. has historically reached only in times of recession or while actively fighting a world war. Under the new administration, interest (both literal and figurative) is only expected to compound as our federal debt is forecasted to pass 128% of GDP by 2035.[17]

In the shadow of these titanic deficits, many investors are starting to reach the same conclusion: the risk-free rate no longer looks quite so risk free. The question now is how much risk is already baked in. This can be measured, albeit somewhat unscientifically, through what’s known as a term premium. “Term premium” is essentially a catch-all phrase to describe all the unknowns that investors expect to get paid for when investing in longer-dated government bonds. This includes things like the expected inflation rate as well as the creditworthiness of the entity issuing the bond. These days, it’s used as a shorthand for faith in the U.S.’s ability to finance its ever-expanding deficit, and investors are concerned that that ability is diminished.

We would argue that investors may not be concerned enough. The Consumer Price Index stands at about 2.7% today. With a yield of 4.6% on the 10-year, that leaves about a 1.9% real term premium. The historical average over the past 50 years pre-Global Financial Crisis, GFC, is around 2.7%, meaning that Treasuries in that context are still a tad expensive. (Breakeven inflation rates are a better gauge of future inflation expectations, but they don’t have as long of a history.) By the Fed’s own admission, inflation is not yet dead and buried, so that will be the likely source of conflict for bond markets over the near term. Looking farther out, the deficit battle will likely reassert itself at some point, but we don’t know when.

In the meantime, we’ve introduced an allocation to gold in our model portfolios to provide exposure to scarce assets. Among other reasons, given the amount of liquidity that’s been injected into the system by virtue of a massive fiscal deficit, we continue to have concerns about the stability of the dollar. Similarly, we see no reason to take long duration risk in fixed income today.

2025 OUTLOOK

Overall, we remain focused on the long-term laws of investing, which tell us that risk management is the key to staying the course. Protecting assets in down years like 2022 helps one stay invested for strong years like 2024

Markets continue to navigate a world defined by shifting geopolitical currents. With slowing growth and easing financial conditions against a backdrop of rising deficits and intensifying protectionist trends, the short-term outlook augurs more volatility ahead. Nevertheless, fundamentals across both consumer and corporate balance sheets remain resilient, and early 2026 earnings forecasts point to robust double-digit growth once again. The short-term implications of each of these different forces in isolation would be nigh upon impossible to ascertain; let alone how they will interact in parallel. We find it to be more fruitful to focus on the longer-term.

One thing we’re always laser-focused on here at AlphaCore is risk management, a principle that tends to come up towards the end of the year as rebalances come to the fore. With one slate of concerns wiped clean and an uncertain future ahead, we believe that it remains crucial to prune any unintended bets in our portfolios and double down on the relationships that we believe will generate our clients’ returns. This includes equities with favorable valuations relative to cash flow growth, alternative credit such as direct lending and structured debt, and multi-strategy hedge funds that can serve as a ballast if public equities retreat. We also find opportunities to go on offense within traditional fixed income given higher absolute yields but remain positioned at the short and intermediate segments of the curve.

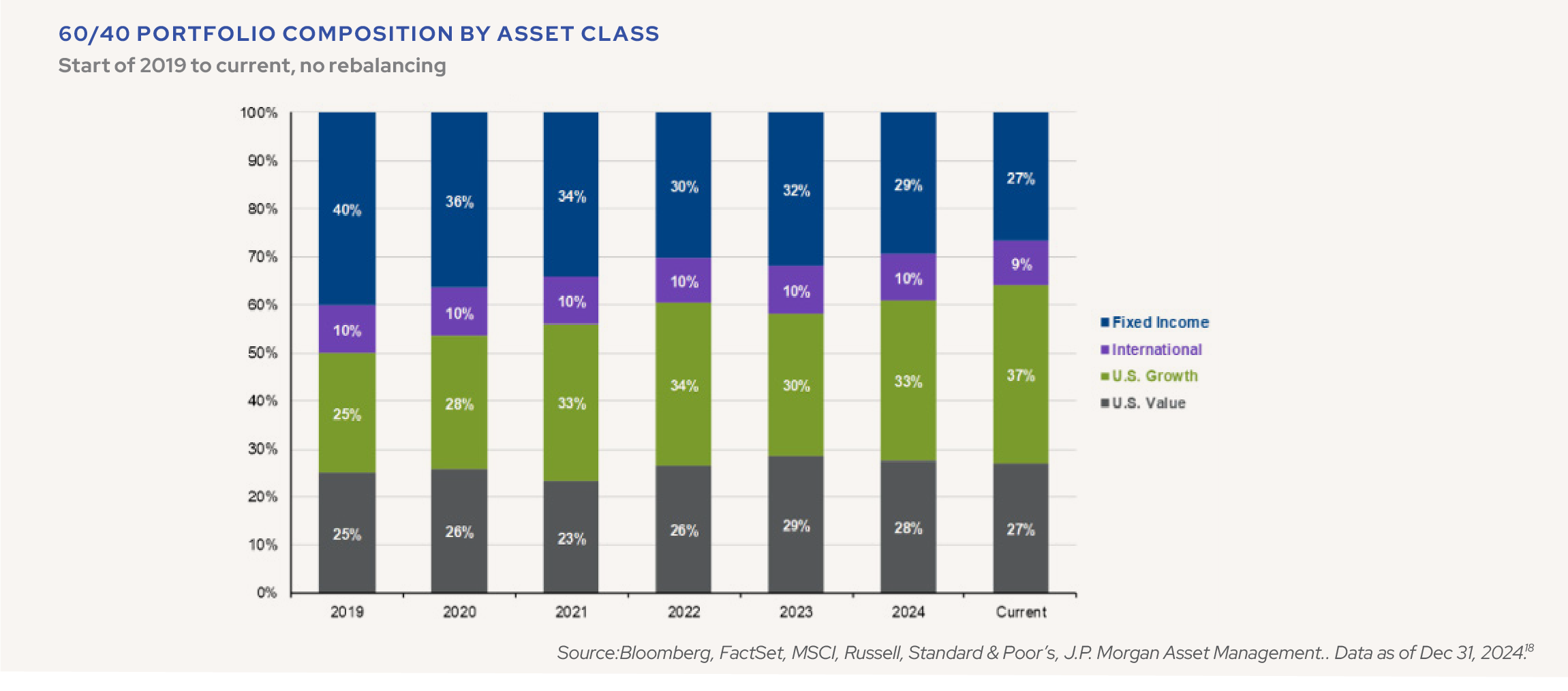

Given that we seek to balance all of these opportunities, it becomes critically important to rebalance. That doesn’t mean it’s always easy to stomach, given that rebalancing necessarily means taking money from our winning ideas and putting it back into those that have struggled. Broad market trends can often persist for multiple years – notably, U.S.-based stocks have outperformed their non-U.S. counterparts by a wide margin over eight of the past 10 calendar years. Looking at even just the past five years, a 60/40 portfolio that failed to rebalance would have seen its international exposure fall — even as equity as a proportion of the overall portfolio grew by 13 percentage points to 73/27.

Source: Source: Bloomberg, FactSet, MSCI, Russell, Standard & Poor’s, J.P. Morgan Asset Management.. Data as of Dec 31, 2024.[18]

True, selling domestic winners to maintain a given weighting in international stocks has not led to better returns. However, abnormal investment relationships tend to revert back to the mean eventually, and investors underestimate this fact at their own peril. With many gains pulled forward and many portfolios likely to be out of whack, we think it makes sense to trim and rebalance and brace for more volatility ahead.

Looking back at 2024 through the prism of history, one cannot help but recall the exuberance and volatility of the original Roaring Twenties. Just as that era saw its share of breakthroughs and imbalances, today’s economic environment reveals a similar interplay between innovation, market dynamism, and structural challenges. For investors, the lessons remain timeless: prudent risk management, disciplined rebalancing, and a focus on long-term fundamentals are as relevant now as they were a century ago. As we navigate the opportunities and uncertainties of the years ahead, we remain steadfast in our commitment to helping our clients weather the ebbs and flows of this modern-day ‘roaring’ decade.

APPENDIX

A few charts we found during the quarter that you may find interesting

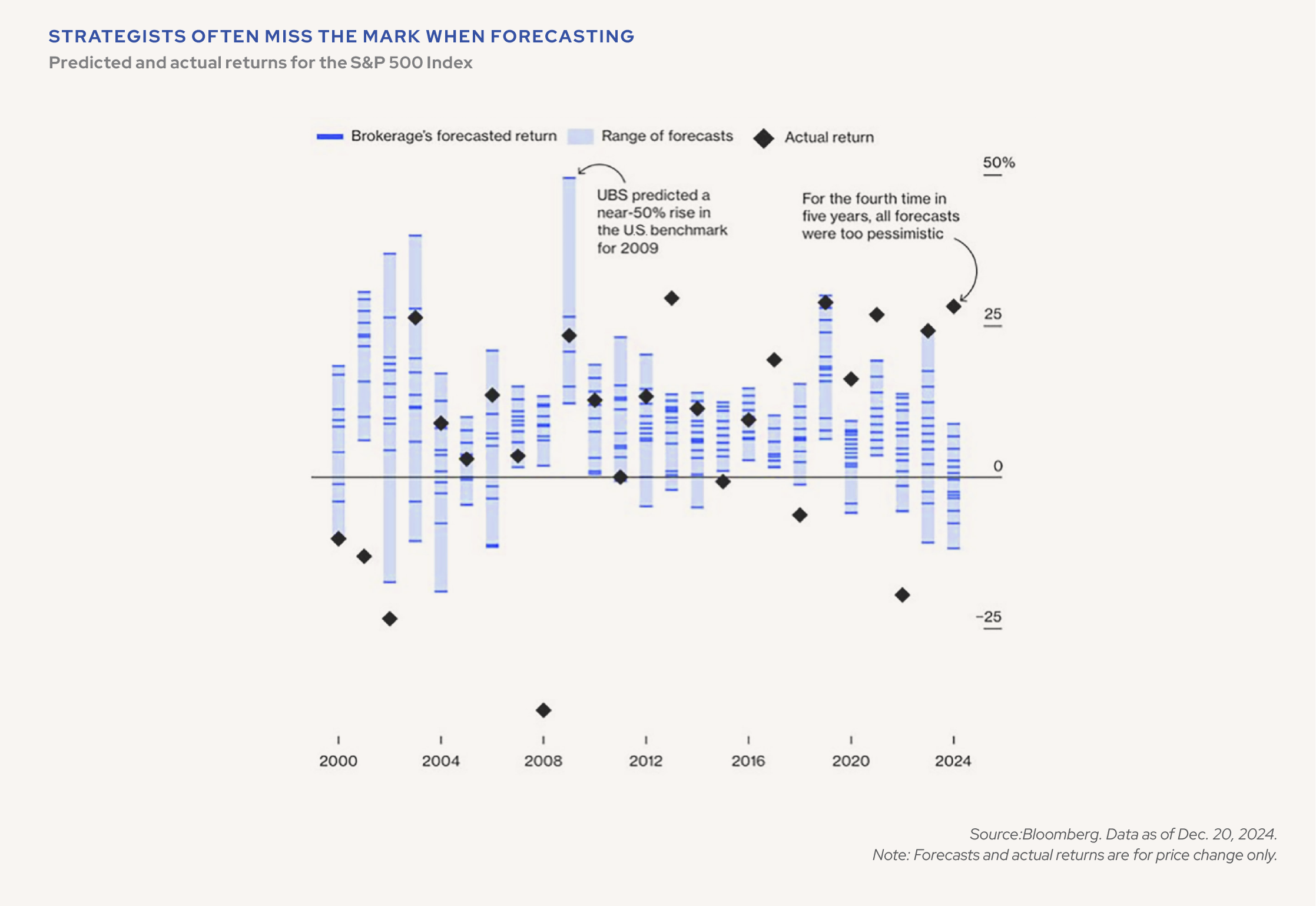

First, a reminder for all watchers of the financial markets, including ourselves. While forecasters often get things directionally right, the magnitude is often wildly off.

Source: Bloomberg. Data as of Dec. 20, 2024.

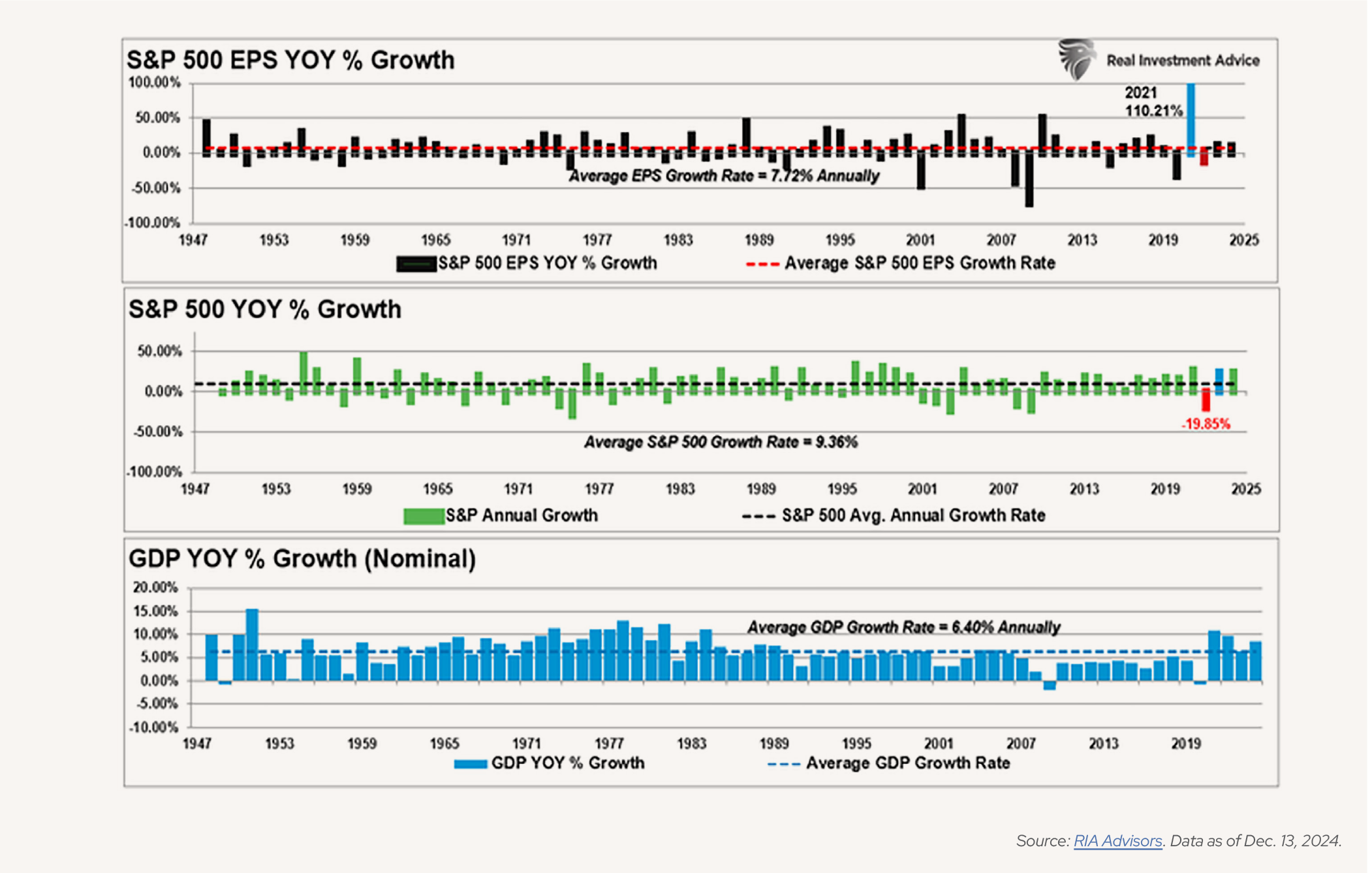

Nevertheless, GDP remains a useful guidepost for assessing earnings trends. Since 1948, a 1% increase in real GDP growth has translated to roughly a 6% increase in S&P 500 earnings on average.

Source: RIA Advisors. Data as of Dec. 13, 2024.

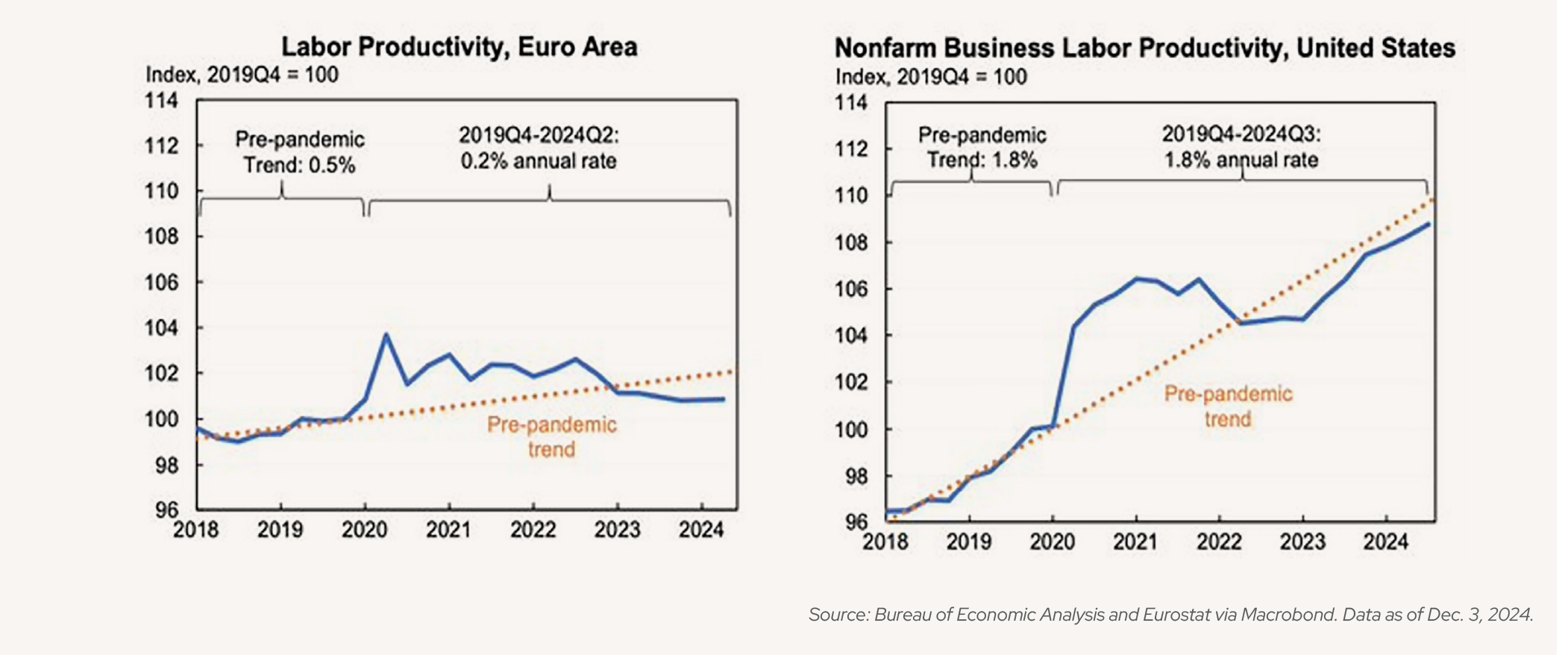

Speaking of GDP, Nonfarm business labor productivity has been a huge driver of the U.S.’s success relative to other developed economies in the post-COVID era.

Source: Bureau of Economic Analysis and Eurostat via Macrobond. Data as of Dec. 3, 2024.

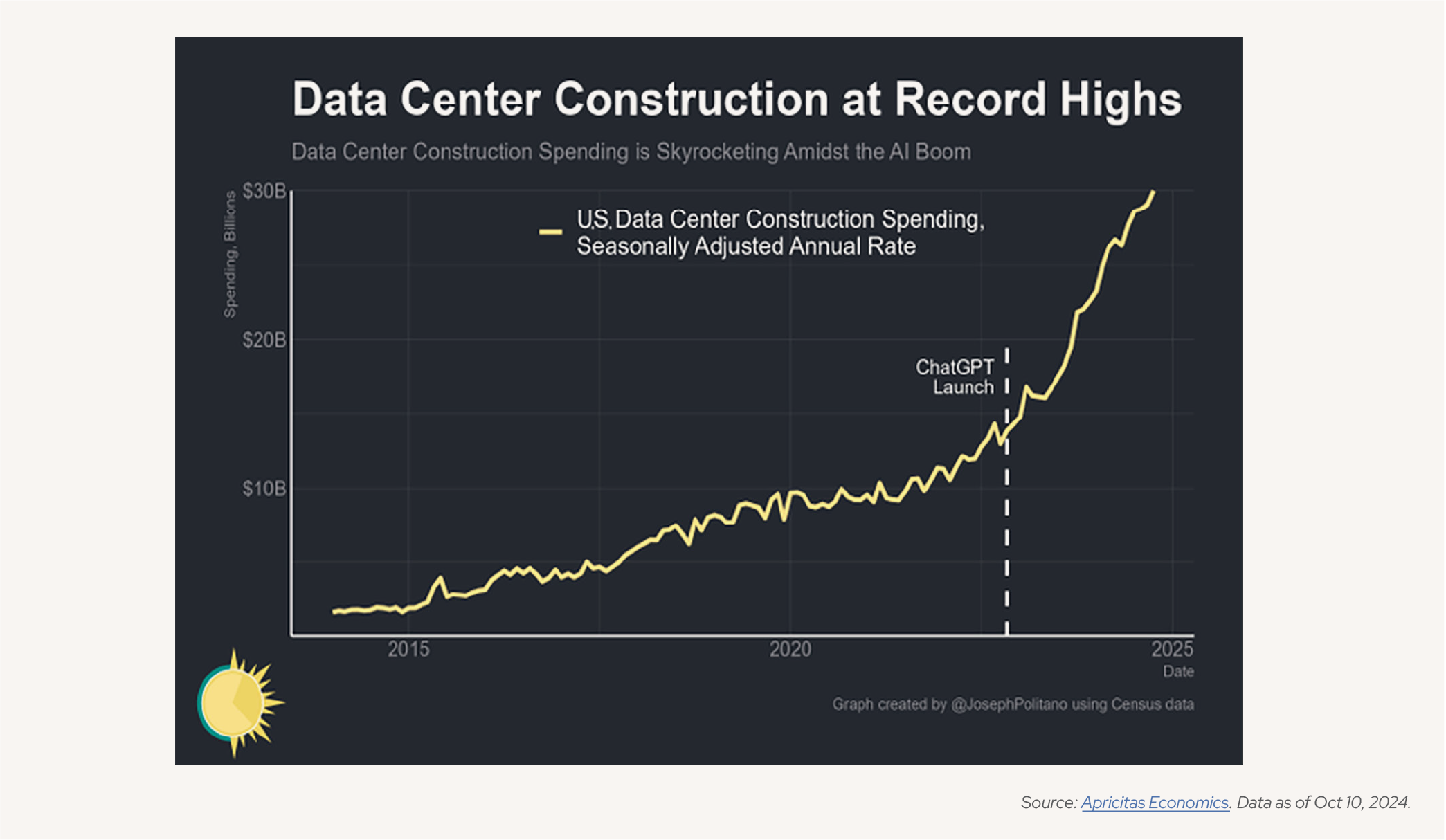

Many market watchers are assuming that data centers will help drive the next productivity boom and building like it.

Source: Apricitas Economics. Data as of Oct 10, 2024.

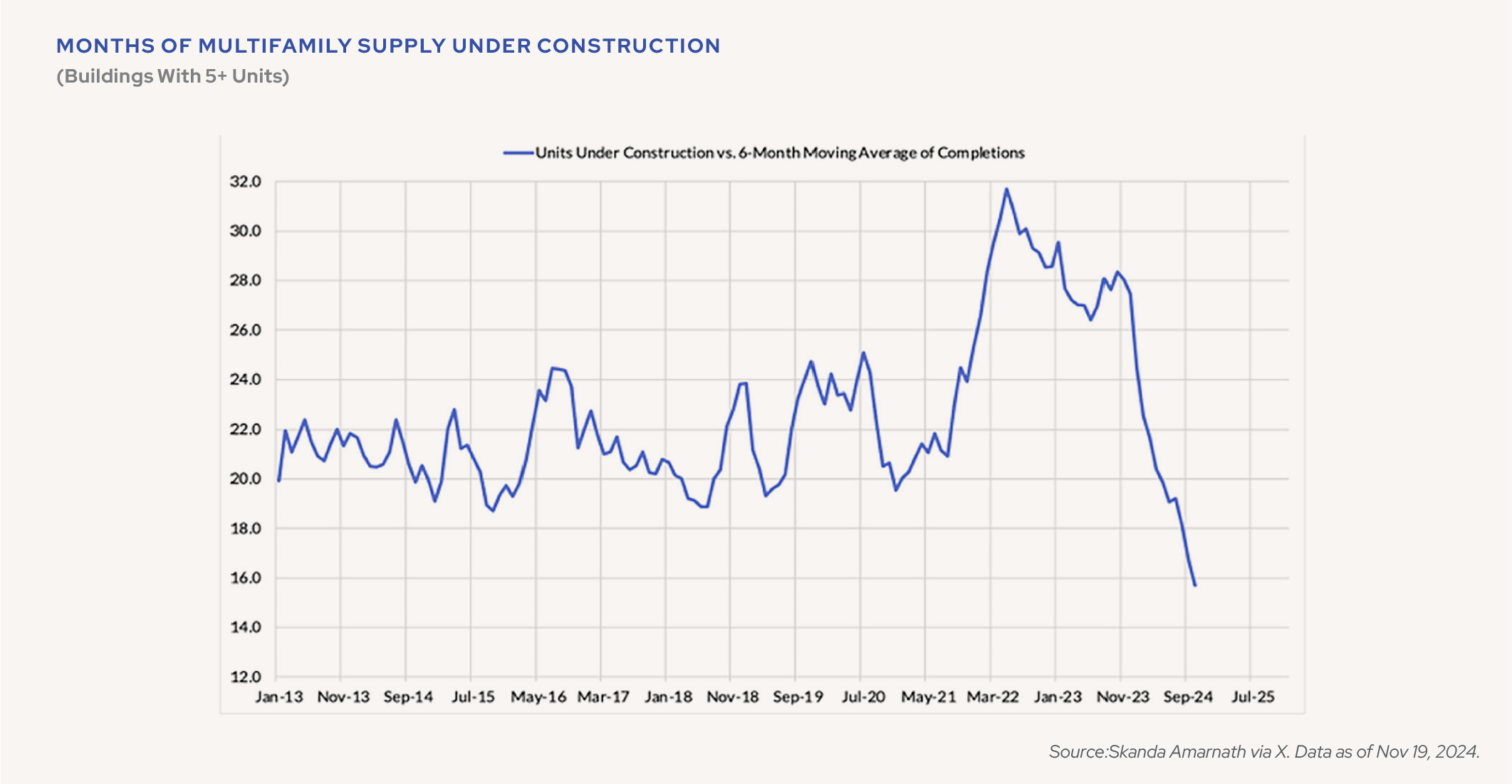

Where real estate developers are NOT building is in multi-family, which is likely to be supportive of higher rents in 2025.

Source: Skanda Amarnath via X. Data as of Nov 19, 2024.

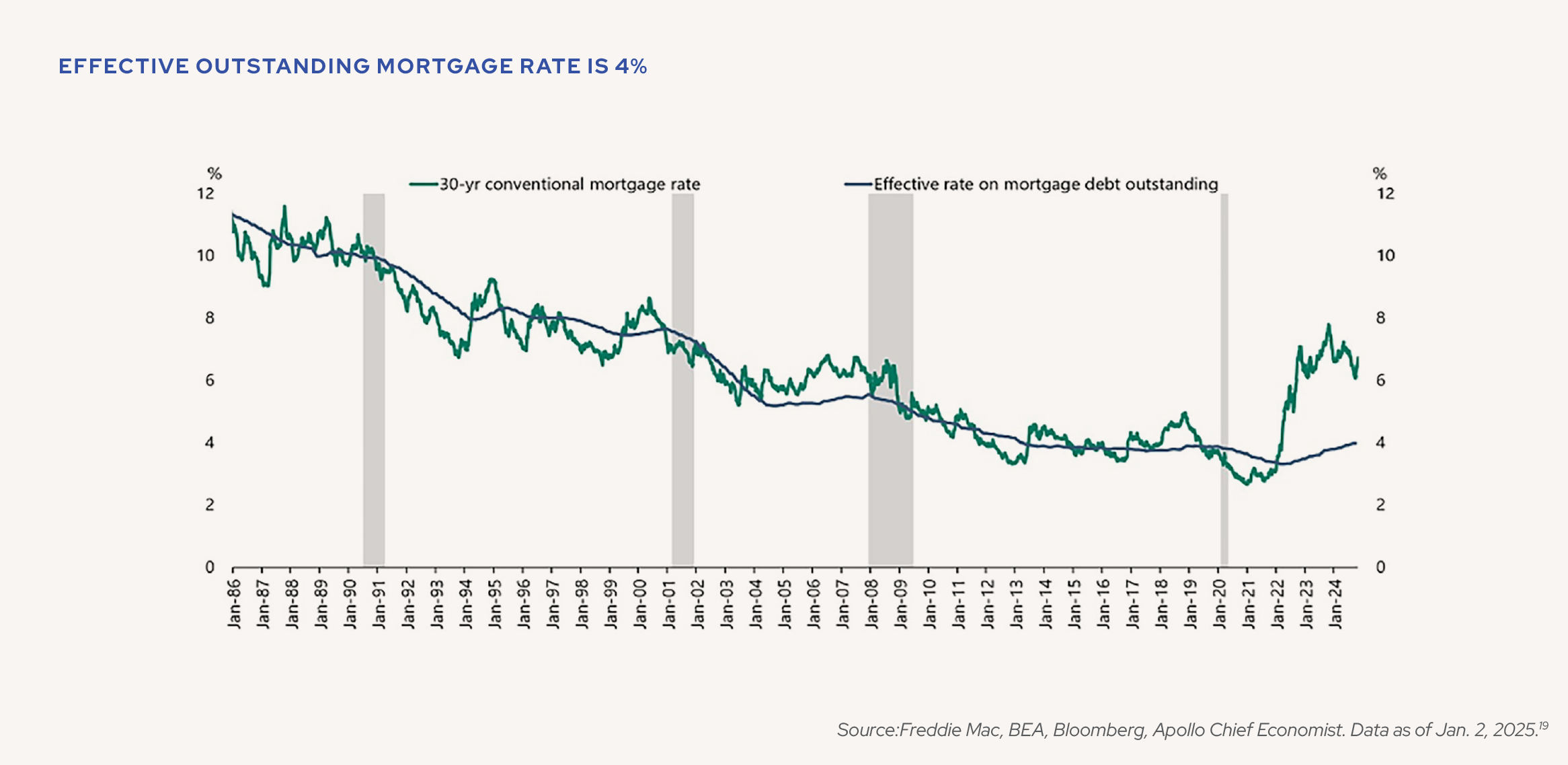

Most homeowners won’t care, though, because they are locked in at very low effective interest rates.

Source: Freddie Mac, BEA, Bloomberg, Apollo Chief Economist. Data as of Jan. 2, 2025.[19]

Neither do corporates, which underscores just how ineffective the Fed’s preferred methods of monetary transmission have been.

Source: Federal Reserve Board, Haver Analytics, Apollo Chief Economist. Data as of Jan. 2, 2025.

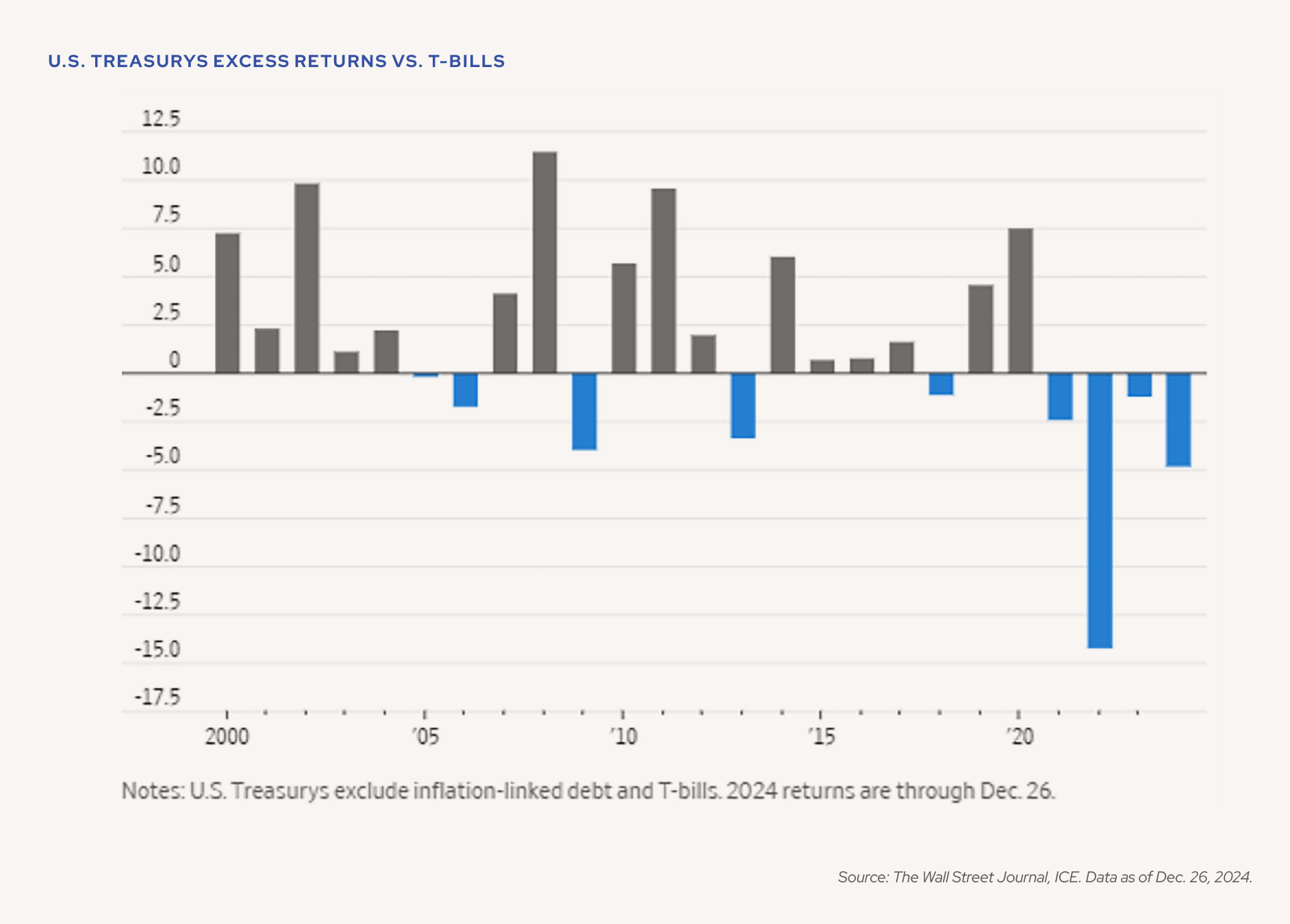

While we’re on monetary transmission… even as the Fed has lowered rates on cash, T-bills have continued to outperform longer-dated notes.

Source: The Wall Street Journal, ICE. Data as of Dec. 26, 2024.

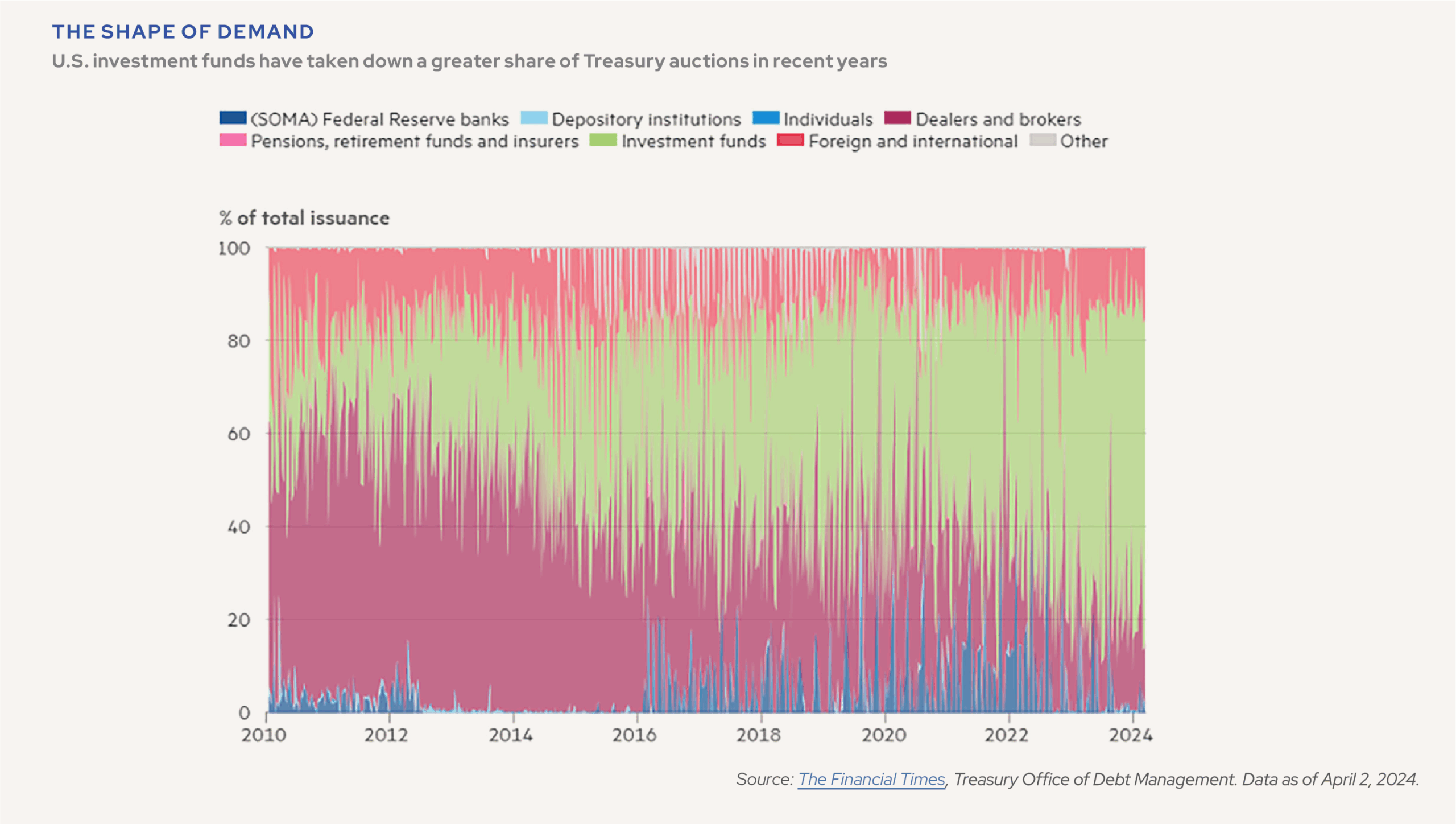

That hasn’t stopped market participants from scooping up the excess issuance, for now. But it has changed who is buying it.

Source: The Financial Times, Treasury Office of Debt Management. Data as of April 2, 2024.

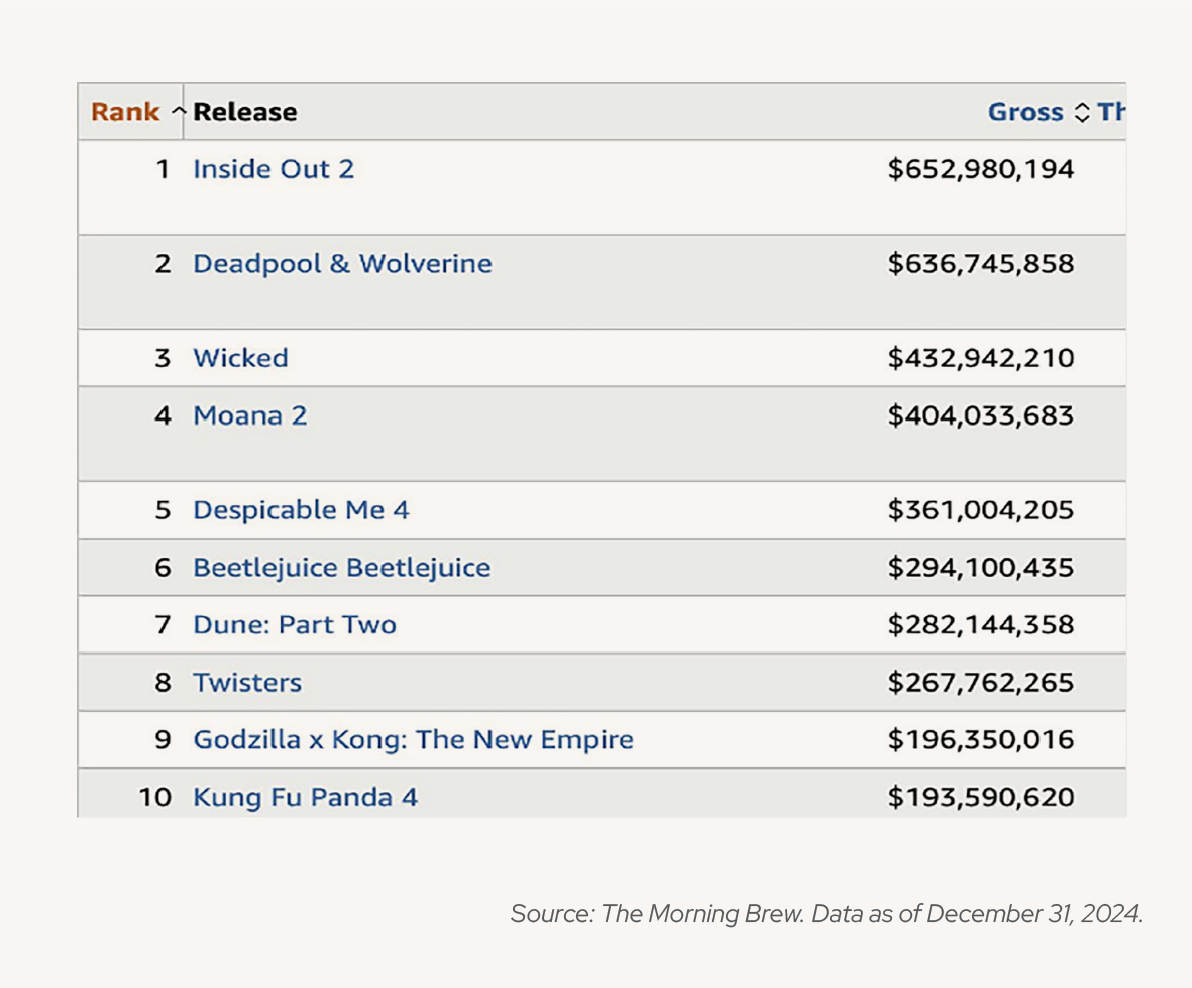

Moving from demand for Treasuries to demand at the box office… of the 10 highest-grossing movies in North America last year, 9 were sequels/reboots…and the 10th was ‘Wicked’

Source: The Morning Brew. Data as of December 31, 2024.

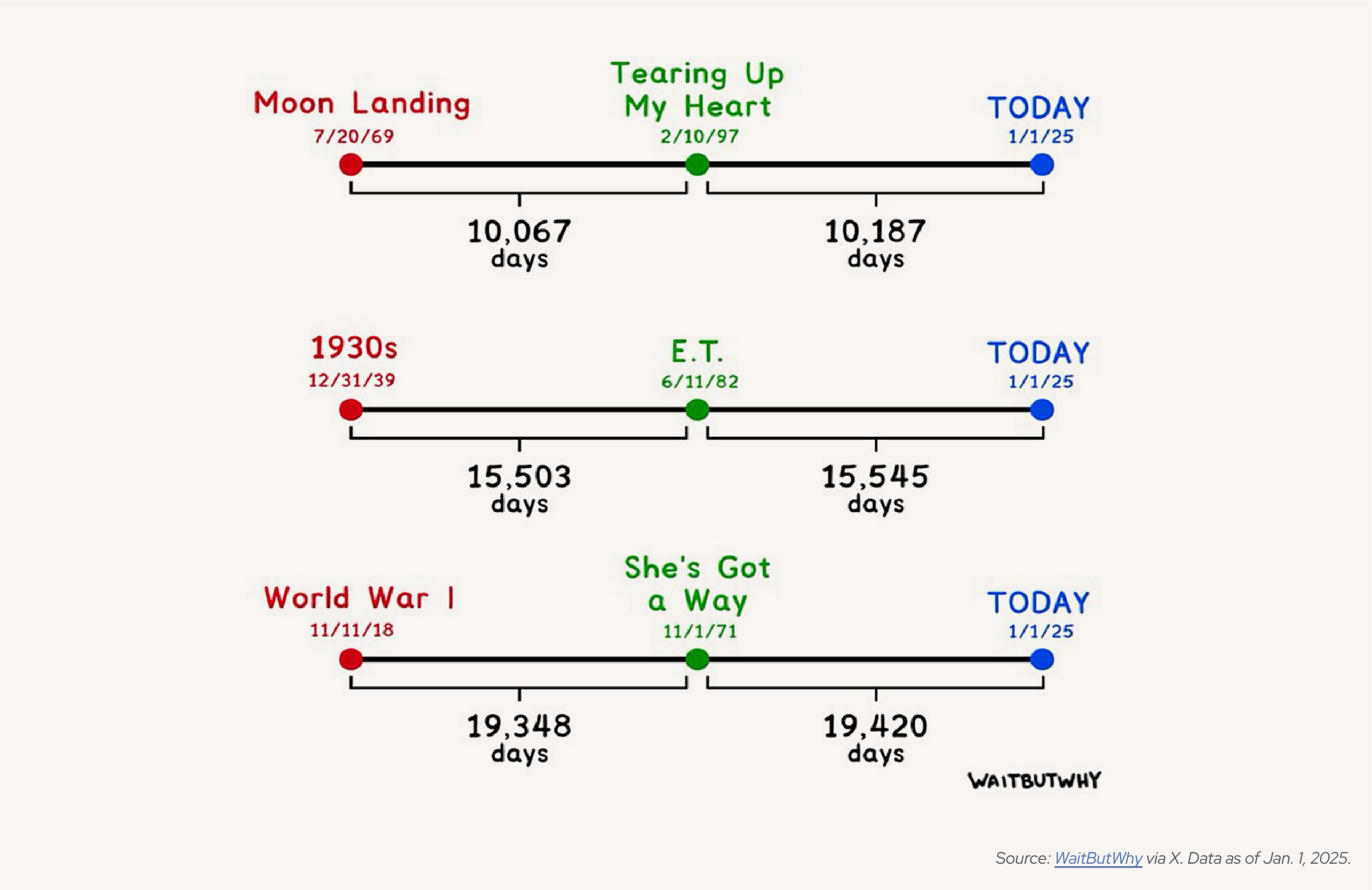

Elsewhere in beloved IP, now that we’ve entered the 2nd quarter of the 21st century (2025-2049), it’s time to update our internal clocks to account for the inexorable passage of time. Until next quarter!

Source: WaitButWhy via X. Data as of Jan. 1, 2025.

MARKET INDICES

BLOOMBERG U.S. AGGREGATE BOND INDEX: The index consists of approximately 17,000 bonds. The index represents a wide range of securities, from investment grade and public to fixed income.

S&P 500 INDEX: S&P 500 index is a float-adjusted market-cap weighted index, largely reflecting the large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

RUSSELL 2000 INDEX: A comprehensive view of small-cap performance, the Russell 2000 measures the performance of approximately 2,000 small-cap U.S. equities.

RUSSELL 1000 GROWTH INDEX: The Russell 1000® Growth Index measures the performance of the large cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000® Growth Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect growth characteristics.

RUSSELL 1000 VALUE INDEX: The Russell 1000® Value Index measures the performance of the large cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The Russell 1000® Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics.

MSCI AWCI EX USA INDEX: The MSCI ACWI ex USA Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the U.S.) and 24 Emerging Markets (EM) countries*. With 2,156 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

MSCI ACWI EX USA US DOLLAR HEDGED: The MSCI ACWI ex USA US Dollar Hedged Index represents a close estimation of the performance that can be achieved by hedging the currency exposures of its parent index, the MSCI ACWI ex USA Index, to the USD, the “home” currency for the hedged index. The index is 100% hedged to the USD by selling each foreign currency forward at the one-month Forward rate. The parent index is composed of large and mid-cap stocks across 22 Developed Markets (DM) countries and 24 Emerging Markets (EM) countries.

WILSHIRE LIQUID ALTERNATIVE INDEX: The Wilshire Liquid Alternative Index℠ measures the collective performance of the five Wilshire Liquid Alternative strategies that make up the Wilshire Liquid Alternative Universe. Created in 2014, with a set of time series of data beginning on December 31, 1999, the Wilshire Liquid Alternative Index platform consists of the Wilshire Liquid Alternative Equity Hedge Index (WLIQAEH), Wilshire Liquid Alternative Global Macro Index (WLIQAGM), Wilshire Liquid Alternative Relative Value Index (WLIQARV), Wilshire Liquid Alternative Multi-Strategy Index (WLIQAMS), and Wilshire Liquid Alternative Event Driven Index (WLIQAED).

ICE U.S. TREASURY 20+ YEAR BOND INDEX: ICE U.S. Treasury 20+ Year Bond Index tracks the performance of U.S. dollar denominated sovereign debt publicly issued by the U.S. government in its domestic market. Qualifying securities must have greater than or equal to twenty years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million. The amount outstanding for all qualifying securities is adjusted to reduce by the amounts held by the Federal Reserve’s SOMA account. Bills, inflation-linked debt, original issue zero coupon securities and STRIPs are excluded from the Index; however, the amounts outstanding of qualifying coupon securities are not reduced by any portions that have been stripped. Agency debt with or without a U.S. Government guarantee and securities issued or marketed primarily to retail investors do not qualify for inclusion in the index.

PERSONAL CONSUMPTION EXPENDITURES (PCE) INDEX: A measure of prices that people living in the United States, or those buying on their behalf, pay for goods and services.

CREDIT SUISSE MANGED FUTURES LIQUID INDEX: The Credit Suisse Managed Futures Liquid Index seeks to gain broad exposure to the Managed Futures strategy using a pre-defined quantitative methodology to invest in a range of asset classes including: equities, fixed income, commodities and currencies. There is a governance framework around the index and it is overseen by an index committee that reviews changes, if any, to the index. Over the index’s history, it has only been modified on a few occasions. Index methodology is confidential and proprietary. In certain circumstances, however, it may be made available upon request and subject to a non-disclosure agreement between the parties.

MSCI EAFE INDEX: The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries around the world, excluding the U.S. and Canada. With 723 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI EAFE 100% HEDGED TO USD INDEX: The MSCI EAFE 100% Hedged to USD Index represents a close estimation of the performance that can be achieved by hedging the currency exposures of its parent index, the MSCI EAFE Index, to the USD, the “home” currency for the hedged index. The index is 100% hedged to the USD by selling each foreign currency forward at the one-month Forward rate. The parent index is composed of large and mid-cap stocks across 21 Developed Markets (DM) countries* and its local performance is calculated in 13 different currencies, including the Euro.

MSCI EMERGING MARKETS INDEX: The MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries*. With 1,253 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI EM U.S. DOLLAR HEDGED INDEX: The MSCI Emerging Markets (EM) U.S. Dollar Hedged Index represents a close estimation of the performance that can be achieved by hedging the currency exposures of its parent index, the MSCI EM Index, to the USD, the “home” currency for the hedged index. The index is 100% hedged to the USD by selling each foreign currency forward at the one-month Forward rate. The parent index is composed of large and mid-cap stocks across 24 Emerging Markets (EM) countries* and its local performance is calculated in different currencies.

RUSSELL 2000 VALUE INDEX: The Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The Russell 2000 Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics.

RUSSELL 2000 GROWTH INDEX: The Russell 2000® Growth Index measures the performance of the smallcap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 2000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect growth characteristics.

BLOOMBERG GLOBAL HIGH YIELD INDEX: The Bloomberg Global High Yield Index is a multi-currency flagship measure of the global high yield debt market. The index represents the union of the U.S. High Yield, the Pan-European High Yield, and Emerging Markets (EM) Hard Currency High Yield Indices. The high yield and emerging markets sub-components are mutually exclusive. Until January 1, 2011, the index also included CMBS high yield securities. The Global High Yield Index is a component of the Multiverse Index, along with the Global Aggregate, Euro Treasury High Yield, and EM Local Currency Government indices. It was created in December 1998, with history backfilled to January 1, 1990.

CONSUMER PRICE INDEX (CPI): The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

HFRI FUND WEIGHTED COMPOSITE INDEX: The HFRI Fund Weighted Composite Index is a global, equal-weighted index of single-manager funds that report to HFR Database. Constituent funds report monthly net of all fees performance in U.S. Dollar and have a minimum of $50 Million under management or a twelve (12) month track record of active performance. The HFRI Fund Weighted Composite Index does not include Funds of Hedge Funds.

COMMENTARY CONTRIBUTORS

Eric Gerster, CFA®

Chief Investment Strategist

Johann Lee, CFA®

Director of Research

Edward J. Durica, III, CFA®

Senior Wealth Advisor

Madeline Hume, CFA®

Senior Research Analyst

IMPORTANT INFORMATION

This material is being provided for informational purposes only. This commentary represents the current market views of the author, and AlphaCore Capital in general, and there is no guarantee that any forecasts made will come to pass. Due to various risks and uncertainties, actual events, results or performance may differ materially from those reflected or contemplated in any forward-looking statements. The opinions are based on market conditions as of the date of publication and are subject to change. No obligation is undertaken to update any information, data or material contained herein.

Neither the information nor the opinions expressed herein constitutes an offer or solicitation to buy or sell any specific security, or to make any investment decisions. AlphaCore provides investment advice only within the context of our written advisory agreement with each AlphaCore client. Past performance is not indicative of future results. The value of an investment may be affected by a variety of factors, including eco- nomic and political developments, interest rates and foreign exchange rates, as well as issuer-specific events.

Any specific security or strategy is subject to a unique due diligence process, and not all diligence is executed in the same manner. All investments are subject to a degree of risk, and alternative investments and strategies are subject to a set of unique risks. No level of due diligence mitigates all risk, and does not eliminate market risk, failure, default, or fraud.

Any securities referenced are solely being used as an illustration of market indices due to availability of current data. This is not intended to reflect securities bought and sold by AlphaCore.

The commentary may utilize index returns, and you cannot invest directly into an index without incurring fees and expenses of investment in a security or other instrument. In addition, performance does not account for other factors that would impact actual trading, including but not limited to account fees, custody and advisory or management fees, as applicable. All of these fees and expenses would reduce the rate of return on investment.

Sources

[1] Survey of Professional Forecasters, Philadelphia Fed. Release date November 15, 2024. https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/survey-of-professional-forecasters

[2] Survey of Professional Forecasters, Philadelphia Fed. Release date November 13, 2023. https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/survey-of-professional-forecasters

[3] Trend growth is measured as the average annual growth rate from business cycle peak 1Q01 to business cycle peak 4Q19.

[4] Recall that when bond yields fall, bond prices rise.

[5] Source: JP Morgan Guide to the Markets. Data as of Jan. 2, 2025.

[6] Source: Morningstar. Data as of Jan. 2, 2025.

[7] Source: Wall Street Journal. Data as of Jan. 2, 2025. https://www.wsj.com/market-data/bonds.

[8] “Terminal rate” refers to the ultimate interest rate that the Federal Reserve sets as its long-term target for federal funds.

[9] Source: Morningstar. Data as of Jan. 3, 2025.

[10] Source: Bloomberg. Data as of Jan. 2, 2025. Multistrategy Hedge Funds From D.E. Shaw to ExodusPoint Delivered in 2024 – Bloomberg

[11] Source: Pitchbook. Data as of Dec. 2, 2024.

[12] Source: U.S. Bureau of Economic Analysis. “Personal Income and Outlays, November 2024.”

[13] Source: BlackRock. Data as of Dec. 4, 2024.

[14] Source: BlackRock, Axios. Calculations are author’s own. Data as of Dec. 26, 2024.

[15] Source: FactSet Earnings Insights. Data as of January 3, 2025.

[16] Source: Vista Equity Partners. Data as of September 30, 2024.

[17] Source: Committee for a Responsible Federal Budget. Data as of July 2024. https://www.crfb.org/blogs/tcja-extension-could-add-4-5-trillion-deficits.

[18] Standard asset allocation at the start of 2019 assumes 60% weight to global equities and 40% to U.S. fixed income. U.S. Value: Equal-weighted Russell 1000 Value and Russell 2000 Value, U.S. Growth: Equal-weighted Russell 1000 Growth and Russell 2000 Growth, International: MSCI ACWI ex-U.S., Fixed Income: 10% Bloomberg Global HY Index and 30% Bloomberg U.S. Aggregate. Past performance is not indicative of future returns.

[19] Note: The effective interest rate (%) reflects the amortization of initial fees and charges over a 10-year period, which is the historical assumption of the average life of a mortgage loan.